Report

The UAE Sustainability Report 2023

Sustainability Trends & Developments in UAE Commercial Offices

November 30, 2023 15 Minute Read

Introduction

Looking for a PDF of this content?

To begin to understand this complex and evolving topic, CBRE has looked at the current state of the sustainable development landscape in the UAE and the progress of planning and implementation of both global and local standards. As a starting point, we focused on the UAE’s commercial office sector, a sector which, both globally and regionally, has been driven to undertake the most rapid rate of compliance with sustainable development and operational standards.

Common International and Local Green Buildings Accreditations

In the UAE, a number of international and local sustainable building certifications and grading schemes have been adopted as the market standards for accreditation. Below, we outline the major characteristics of each of these standards. After an initial assessment of asset certifications, we found LEED to be the most commonly adopted certification scheme. Hence, we have focused on assets that are LEED-certified when calculating premiums associated with sustainable developments.

Impact on the UAE’s Office market

The occupiers drive to sustainability

Abu Dhabi

Historically, demand for green-certified spaces in Abu Dhabi’s office market had been relatively restrained as long-standing demand occupier groups seldom had among their top requirements office space which had green certifications. Alongside changes in regulations, such as the introduction of Estidama in 2010, growth in new office developments, and relocation activity from global and local sources, all underpinned by growing levels of demand for green-certified commercial spaces, we saw the introduction of developments directly catering to these requirements. The first of which was the introduction of Siemens Headquarters in Masdar City in 2014 which became Abu Dhabi’s first Platinum LEED-certified development. From this period onwards, we have seen a number of other developers not only adopt the minimum rating criteria but, in most cases, far exceed the baseline.

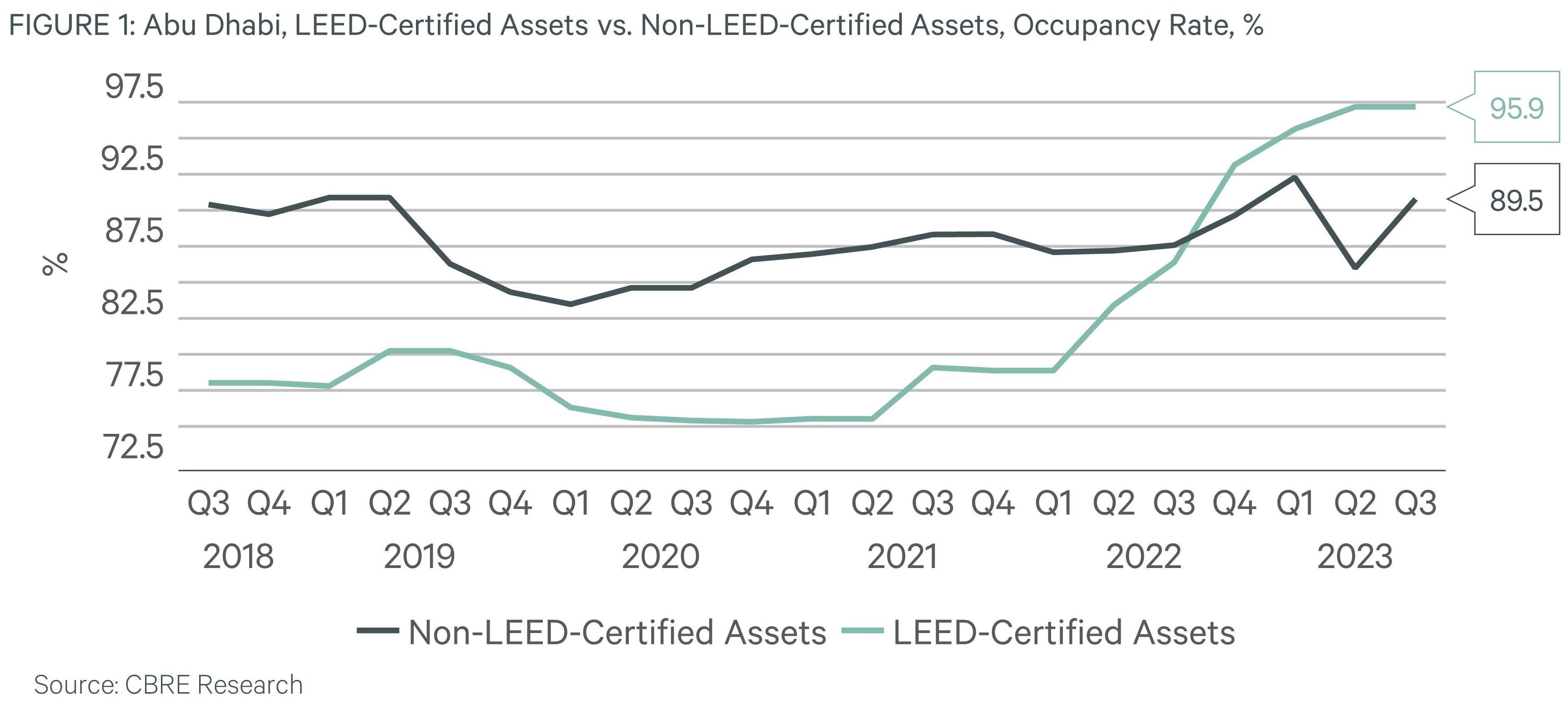

Most recently, as more private sector companies look to either establish or increase their footprint within the capital, we have seen demand for green accredited assets only continue to increase. Currently, LEED-certified developments account for 50.3% of the total gross leasable area (GLA) of institutional-grade buildings that CBRE tracks. This amounts to a total of 445,649 square metres. As a result, the average occupancy rate of LEED-certified assets increased from 85.1% in Q3 2022 to reach 95.9% as at Q3 2023. Over this period, the occupancy rate of non-LEED-certified developments stood at 89.5%, up from 86.3% compared to the year prior.

LEED-certified assets have always registered a significant outperformance compared to non-LEED-certified assets by achieving higher rental rates, not only due to the elevated levels of demand but also given the premium quality of these assets. In Q3 2023, the premium for LEED-certified buildings compared to non-LEED-certified buildings stood at an average of 33.0%.

Increased adoption of LEED

Dubai

In the recent past, cost consideration had been one of the primary drivers in Dubai’s occupier market. This, combined with an extremely limited supply of LEED-accredited spaces, meant that there were no discernible trends to note when in relation to premiums achievable for LEED-accredited stock. With the introduction of new stock and the increased prevalence of flight to quality, stemming largely from the pandemic, we have not only seen demand for such accredited spaces increase but also have seen landlords actively looking to meet the criteria required for accreditation.

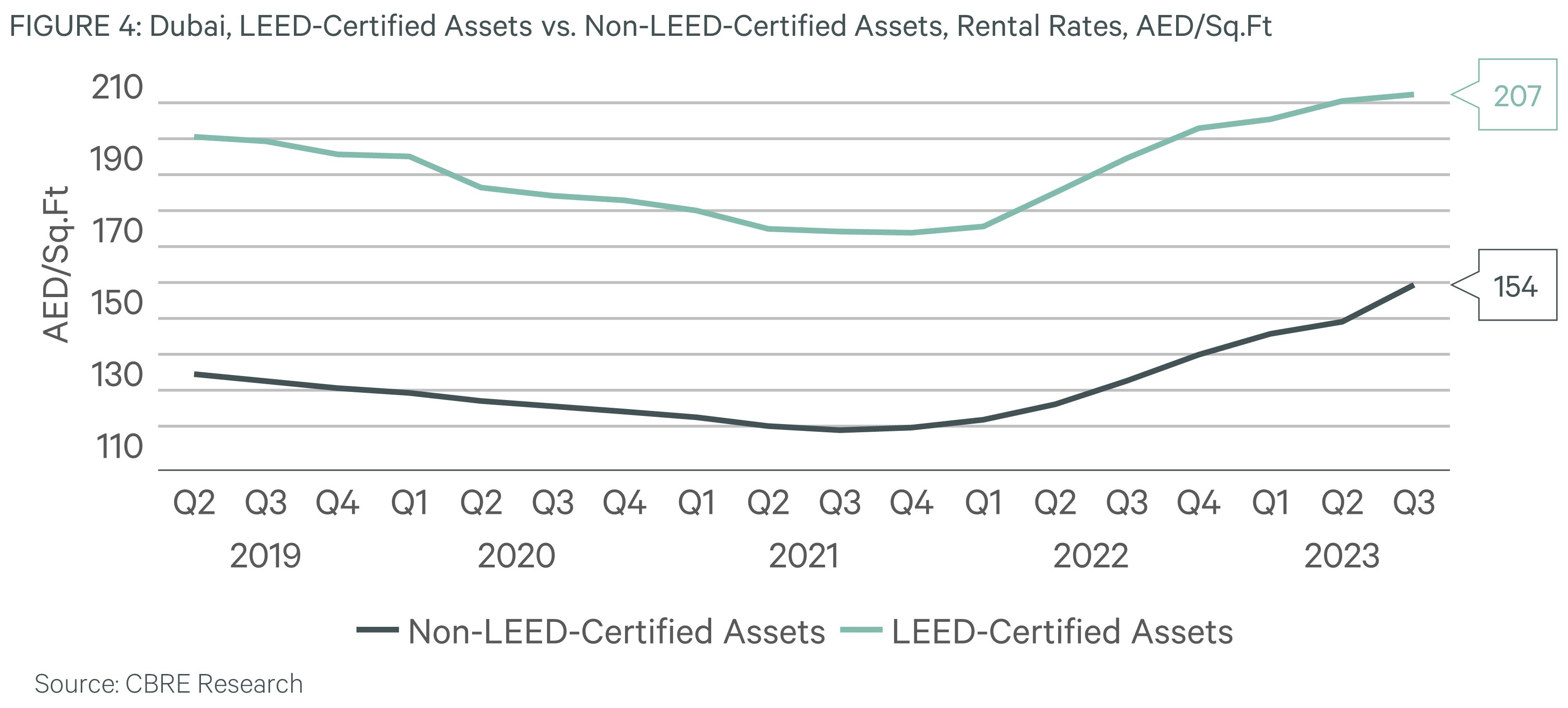

Some 73.1% of the assets we have identified as LEED-Gold and above were accredited from 2020 onwards. Currently, 23.7% of the total gross leasable area of assets that CBRE monitors are LEED-certified, reaching a total of 12.2 million square feet of LEED-accredited space. The average occupancy rate of these assets, as at Q3 2023, stood at 96.2%, up from 91.1% a year earlier. Throughout the same period, the average occupancy rate of non-LEED-certified assets reached 90.6%, up from 85.2% compared to Q3 2022. As can be seen in Figure 3, there has been a clear divergence in performance between the two groupings from 2021.

Given these elevated levels of demand and the generally higher quality of such developments, these LEED-certified assets, on average, were able to command higher rental rates compared to non-LEED-certified assets. As at Q3 2023, the average premium for LEED-certified assets reached 34.3%. More so, whilst the data to support the argument is still nascent, we note a distinct relationship, where the higher the LEED rating for assets, the higher the premium they can achieve.

LEED premium occurs even at a micro level

Dubai

Given the nature of Central Business District (CBD) clusters in Dubai and the various intricacies associated with each of these clusters, it is important to also analyse the premium rates of rent that LEED-certified buildings are able to achieve in relation to non-certified buildings within their cluster.

Firstly, in key commercial hubs that are home to some of Dubai’s most prominent Prime and Grade A assets, LEED-certified buildings have almost uniformly achieved at least the same rate as non-certified buildings, with Downtown Dubai being the only exception. However, in most cases, these Prime and Grade A assets were able to secure significantly higher rental rates compared to non-LEED-certified developments within their respective clusters. As at Q3 2023, certified assets in the likes of Dubai Silicon Oasis, Trade Centre District, DIFC Northern Precinct, and TECOM Freezone registered average premiums of 128.4%, 51.4%, 23.9%, and 13.0%, respectively.

In most cases, LEED-certified Prime and Grade A assets were able to secure significantly higher rental rates compared to non-LEED-certified developments within their respective clusters.

Sustainable development practices are not a choice

This research makes a strong case for LEED-accredited developments, whilst, for new developments, accreditation is non-negotiable, we can also begin to establish this being the case for existing developments, where this is likely to become the status quo. Going forward, we expect that the premium between accredited and non-accredited buildings will only continue to expand up to the point where non-accredited buildings will effectively become obsolete.

Going forward, we expect that the premium between accredited and non-accredited buildings will only continue to expand up to the point where non-accredited buildings will effectively become obsolete.