Article

Is there a supply crisis in Dubai’s office market?

Dubai is witnessing a ‘first come, first served’ leasing mentality, as good quality office space faces long-term supply issues.

December 12, 2023

Crisis is a word that I don’t use lightly, however we are seeing a significant shortage of good quality Grade A office space within the Dubai market currently, with no signs of any relief in the short to medium term.

You would have to cast your minds back almost 10 years to find a similar scenario to the one that Dubai is currently facing. However, the pace in which we’ve seen absorption over the last 12-24 months is unparalleled. This is completely new territory that hasn’t been experienced previously and is something that tenants, both regional and multinational, are struggling to come to terms with.

You wouldn’t have to look too far back to find a market that was facing massive oversupply issues, plummeting rental rates and extensive lease incentives being offered by landlords in order to capture strong covenant tenants within their portfolios. Desperation was particularly evident with private/strata landlords who were almost creating a race to the bottom to simply fill their vacant space and cover their operating costs, offering rents as low as AED 40 – 60 per sq ft per annum.

These times already feel like a distant memory with landlords now being extremely bullish with their commercial proposals and are significantly rolling back incentives and flexibility within leases post-pandemic. Despite this aggressive approach, tenants are snapping up available space within record time, often not even allocating sufficient time to undertake the necessary due diligence on a unit/location in order to ensure that they do not miss out on their preferred options. Tenants are being expected to sign offers and leases in time periods that they simply aren’t comfortable with as landlords are adopting a first come, first served approach, which is something that we haven’t seen in the Dubai market for many years.

As it stands, there are a handful of schemes across the Dubai market that are able to offer a large quantum of Grade A office space and unsurprisingly, this is from large institutional developers who understand the market dynamics and cycles in which Dubai operates. Expo City and Dubai Commercity are two great examples of schemes that either have existing vacancy or upcoming vacancy in line with their development plans. Both are high-profile and offer tenants a low-rise business park/campus feel with a plethora of amenities onsite or nearby. A product that is proving very popular currently.

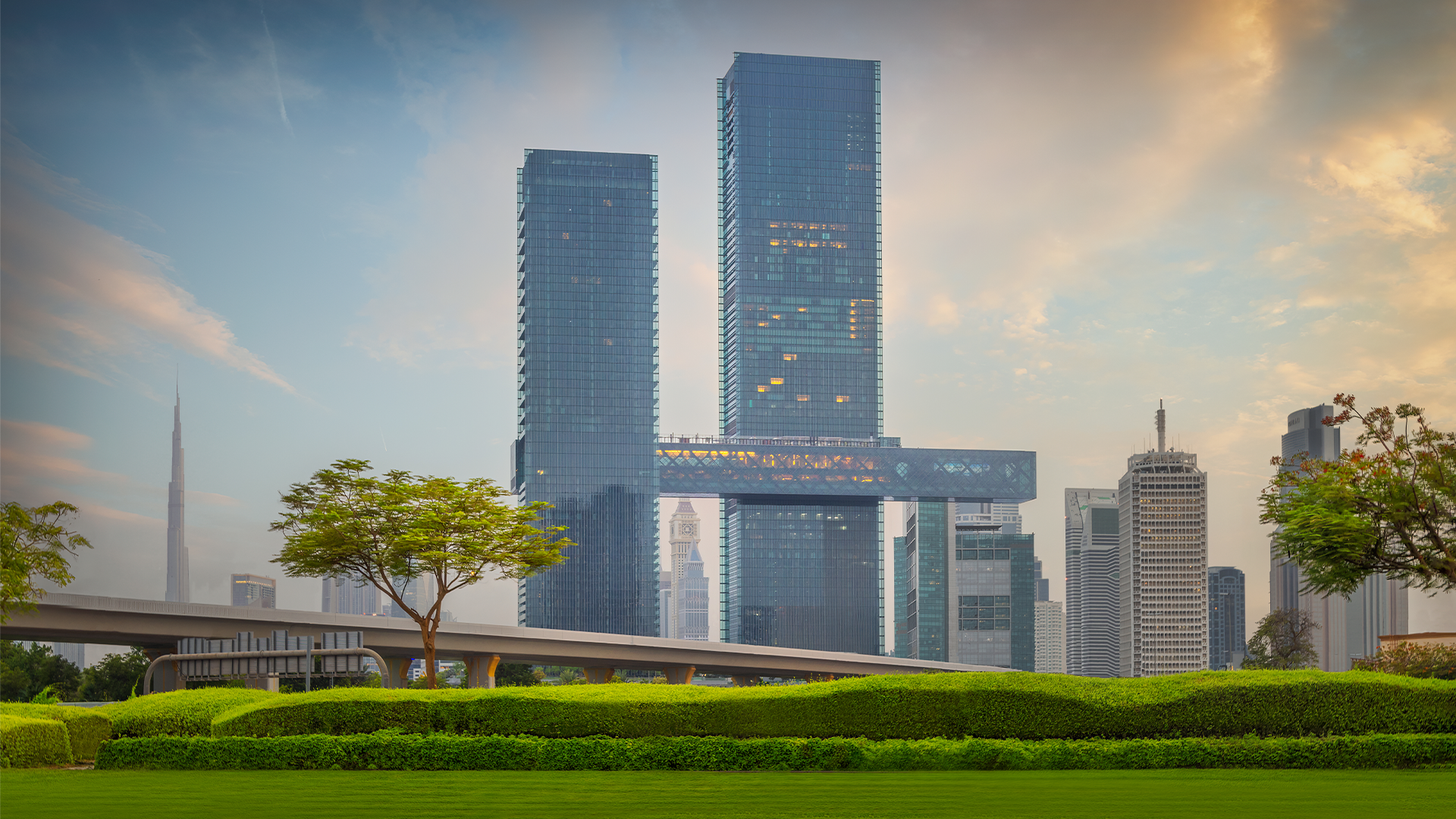

The newest addition to the Dubai office landscape is The Offices at One Za’abeel of which CBRE has recently been appointed on a joint exclusive basis. This premium asset is about to launch its office component, releasing approx. 280,000 sq.ft. of Grade A office space to the market at rental levels in the range of AED 275 – 325 per sq ft per annum. Whilst this is a welcome relief, given the high-profile nature of this asset, the highly efficient floorplates and level of demand that CBRE is already experiencing, we expect the office component to be fully leased by the end of 2024, thus not really addressing the long-term supply issues forecasted.

So, what does this mean for companies looking to upgrade their premises or seek new office accommodation over the next two to three years until the next significant wave of supply is due to be delivered? Whilst a challenging question to answer, it’s not all doom and gloom as we envisage a healthy amount of churn across the large institutional assets, providing companies with options, albeit limited, to relocate/consolidate. With high occupancy levels likely to remain for the foreseeable, this will have a knock-on impact on rental rates, with landlords all too aware of the supply/demand balance as it currently stands. Average rents within the Prime and Grade A segments reached AED 249 and AED 178 per sq ft per annum respectively, which, compared to the levels we saw back in 2019 for example which would have been ranging from AED 90 – 175 per sq ft per annum respectively, shows significant growth across the market over the last few years. Whilst we are seeing sharp increases in rents in Dubai, its Prime rents still sits comfortably below other international hub cities. As at Q3 2023, average Prime rents in Dubai, in US dollar terms stood at $68.7 per square foot per year, in the likes of London City, London West End and Singapore, the comparable figures stand at $90.1, $170.4 and $106.7 per square foot per year respectively. Given the somewhat substantial discounts that Dubai’s Prime office market has to offer, alongside the business and lifestyle offerings, its office market is more than competitive on a global level.

We also expect to see an influx of sub-lease space being introduced to the market over the course of the next 12-24 months. This will come primarily from multinational and regional corporates who have surplus space within their office portfolios and who are committed to long-term leases and subsequently need to find alternative solutions to cover their occupancy costs. We saw a significant amount of sub-lease space enter the market soon after the pandemic. That space was leased very quickly, as it is often offered in a fully fitted (plug & play) handover condition at very attractive rental rates, in line with the tenant’s master lease. Given some of the global headwinds that multinational corporates are currently facing as well as the forecasted economic slowdown that is likely to trickle into 2024, we expect a range of corporates to act accordingly and look at ways to reduce their liability and provision for long-term sustainability and growth.

In summary, a challenging time ahead for companies seeking good quality space in particular. Available space will be sparse and expensive, however, opportunities are likely to arise in this dynamic market, as they always seem to in Dubai. Companies will need to remain extremely agile if they’re to benefit from these opportunities, something that many find challenging in the current global climate.

First come, first served

With schemes such as ICD Brookfield Place, DWTC One Central and DMCC Uptown Tower all reaching major milestones of being fully leased over the last 12 months, this has had a huge impact on potential relocation options for our corporate clients.You wouldn’t have to look too far back to find a market that was facing massive oversupply issues, plummeting rental rates and extensive lease incentives being offered by landlords in order to capture strong covenant tenants within their portfolios. Desperation was particularly evident with private/strata landlords who were almost creating a race to the bottom to simply fill their vacant space and cover their operating costs, offering rents as low as AED 40 – 60 per sq ft per annum.

These times already feel like a distant memory with landlords now being extremely bullish with their commercial proposals and are significantly rolling back incentives and flexibility within leases post-pandemic. Despite this aggressive approach, tenants are snapping up available space within record time, often not even allocating sufficient time to undertake the necessary due diligence on a unit/location in order to ensure that they do not miss out on their preferred options. Tenants are being expected to sign offers and leases in time periods that they simply aren’t comfortable with as landlords are adopting a first come, first served approach, which is something that we haven’t seen in the Dubai market for many years.

Long-term supply issues ahead

Whilst occupancy levels are high across institutional grade assets, currently at 92.4%, there is still sufficient space in the market to place our corporate clients. However, this availability is reducing week by week and the bigger challenge is now just around the corner, as we’re likely to be facing serious supply shortages in 2024 and onwards. With only around 1.4 million sq.ft. of office supply scheduled to be brought online in the Dubai market in the next three years or so, this simply won’t be sufficient to cater to the current levels of demand that we’re currently facing. Particularly as the majority of this space already has pre-lease commitments in place. Whilst we expect demand to begin to taper off slightly in 2024, it certainly won’t be to the levels required to meet the vacancy being offered in the market over the next few years.As it stands, there are a handful of schemes across the Dubai market that are able to offer a large quantum of Grade A office space and unsurprisingly, this is from large institutional developers who understand the market dynamics and cycles in which Dubai operates. Expo City and Dubai Commercity are two great examples of schemes that either have existing vacancy or upcoming vacancy in line with their development plans. Both are high-profile and offer tenants a low-rise business park/campus feel with a plethora of amenities onsite or nearby. A product that is proving very popular currently.

The newest addition to the Dubai office landscape is The Offices at One Za’abeel of which CBRE has recently been appointed on a joint exclusive basis. This premium asset is about to launch its office component, releasing approx. 280,000 sq.ft. of Grade A office space to the market at rental levels in the range of AED 275 – 325 per sq ft per annum. Whilst this is a welcome relief, given the high-profile nature of this asset, the highly efficient floorplates and level of demand that CBRE is already experiencing, we expect the office component to be fully leased by the end of 2024, thus not really addressing the long-term supply issues forecasted.

Sub-lease space may be the answer

So, what does this mean for companies looking to upgrade their premises or seek new office accommodation over the next two to three years until the next significant wave of supply is due to be delivered? Whilst a challenging question to answer, it’s not all doom and gloom as we envisage a healthy amount of churn across the large institutional assets, providing companies with options, albeit limited, to relocate/consolidate. With high occupancy levels likely to remain for the foreseeable, this will have a knock-on impact on rental rates, with landlords all too aware of the supply/demand balance as it currently stands. Average rents within the Prime and Grade A segments reached AED 249 and AED 178 per sq ft per annum respectively, which, compared to the levels we saw back in 2019 for example which would have been ranging from AED 90 – 175 per sq ft per annum respectively, shows significant growth across the market over the last few years. Whilst we are seeing sharp increases in rents in Dubai, its Prime rents still sits comfortably below other international hub cities. As at Q3 2023, average Prime rents in Dubai, in US dollar terms stood at $68.7 per square foot per year, in the likes of London City, London West End and Singapore, the comparable figures stand at $90.1, $170.4 and $106.7 per square foot per year respectively. Given the somewhat substantial discounts that Dubai’s Prime office market has to offer, alongside the business and lifestyle offerings, its office market is more than competitive on a global level.We also expect to see an influx of sub-lease space being introduced to the market over the course of the next 12-24 months. This will come primarily from multinational and regional corporates who have surplus space within their office portfolios and who are committed to long-term leases and subsequently need to find alternative solutions to cover their occupancy costs. We saw a significant amount of sub-lease space enter the market soon after the pandemic. That space was leased very quickly, as it is often offered in a fully fitted (plug & play) handover condition at very attractive rental rates, in line with the tenant’s master lease. Given some of the global headwinds that multinational corporates are currently facing as well as the forecasted economic slowdown that is likely to trickle into 2024, we expect a range of corporates to act accordingly and look at ways to reduce their liability and provision for long-term sustainability and growth.

In summary, a challenging time ahead for companies seeking good quality space in particular. Available space will be sparse and expensive, however, opportunities are likely to arise in this dynamic market, as they always seem to in Dubai. Companies will need to remain extremely agile if they’re to benefit from these opportunities, something that many find challenging in the current global climate.

Contact Us

Stay Connected

Receive relevant research reports, thought leadership, invitations to CBRE events and more.

Connect with an Expert

Share a few details about your request to get started with our team.