Dubai Residential Market Notes

Transaction volumes continue to soar and reach new records

July 1, 2024

Higher demand is underpinning strong absorption levels

Much has been said about the influx of new launches and the potential dampening impact that this may have on prices, where supply may again start to outweigh demand. However, the absorption of new stock sits at markedly high levels, where our headline analysis shows at least 70.0% of units which were launched since 2022, have been sold to date, due to lags in data, we anticipated that this number is materially higher. More so, within Dubai’s core and established residential areas, this figure is, on average, well above 80.0%. Anecdotally, we are seeing that a considerable portion of this demand in the off-plan market is originating from owner-occupiers, therefore, in the longer term, we expect that the increase in supply will provide some relief to the rental market, but for sales prices, it is unlikely to create downward pressure.

Source: CBRE Research/ REIDIN

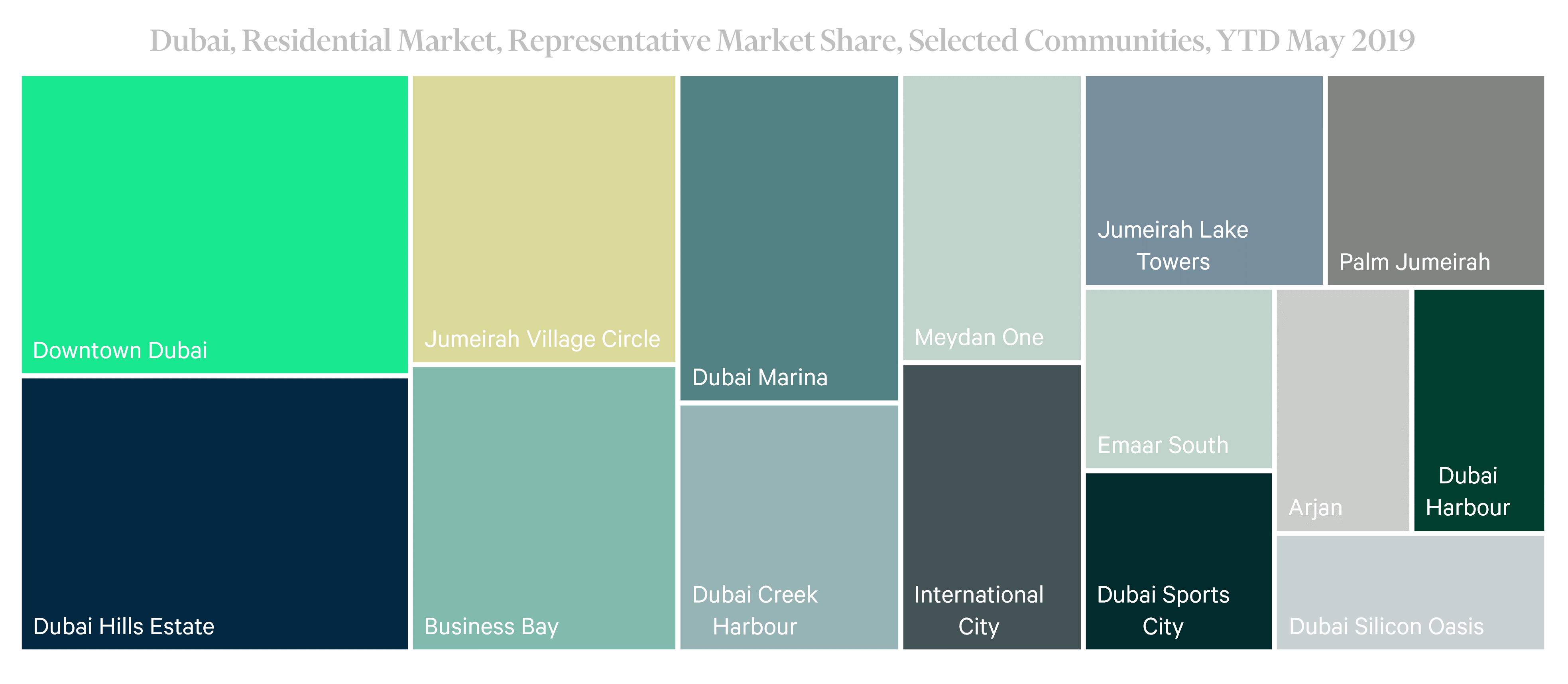

Moving to the ‘burbs

Source: CBRE Research/ REIDIN

Source: CBRE Research/ REIDIN

Source: CBRE Research/ REIDIN

It’s not all about Prime

Unsurprisingly, we are seeing a significant upward shift in which price brackets that transactions are happening, but the importance of and available opportunities in the affordable and core market segments cannot be understated.In May 2024, the number of transactions priced below AED 1,000 per square foot registered a decline of 19.3% from the comparable period a year earlier, standing at a total of 2,417, which accounts for 15.3% of May’s total sales level.

The core market continues to grow and has seen a marked year-on-year increase of 64.1% in the number of transactions priced between AED 1,000 and AED 2,000 square foot in May 2024, reaching a total of 8,247, this accounts for 52.3% of the total transactions registered in the month of May. Given the upward pressure on prices and strong demand for upper-mid-end properties, the AED 2,000 and AED 3,000 bracket, which currently amounts to 25.6% of the total number of residential transactions, registered an increase of 154.0% in activity levels in the 12 months to May 2024, with transactions in this segment totalling 4,034 as at May.

In the higher-end segments of the market, the lack of available stock, particularly in prime and super-prime areas is impacting activity level. Sales of residential properties priced between AED 3,000 and AED 8,000 per square foot, which accounts for 6.6% of the total number of transactions in May 2024, registered a drop of 19.5% from the previous year. Residential properties priced at AED 8,000 per square foot and above only represent 0.2% of total sales registered in May 2024, down from 0.3% a year earlier, owing to the limited levels of demand and availability of such assets.

Source: CBRE Research/ REIDIN

Price growth is expected to remain fairly strong into the second half of 2024

Elevated levels of activity have also continued to underpin stronger than expected price growth, that being said, we have started seeing a slight moderation in the pace of growth, however we expect that by the end of 2024, the moderation will only be slight.In May 2024, average residential prices in Dubai registered a year-on-year increase of 20.1%, down from the 20.7% growth recorded a month earlier. Over this period, average apartment prices increased by 19.8% to stand at an average of AED 1,530 per square foot, and average villa prices increased by 21.8% to reach AED 1,847 per square foot. In both the apartment and villa segments of the market, Palm Jumeirah recorded the highest sales rates per square foot, with average rates reaching AED 2,804 and AED 5,228, respectively, as of May 2024.

We are beginning to see some market stability begin to take hold

As mentioned, price performance is expected to remain strong over the upcoming period in both the apartment and villa segments of the market, although the market seems to be finding some stability. The latest listings data shows that in the year to date to May 2024, 88.4% of listings’ prices have remained unchanged, up from 79.7% over the same period a year earlier. During the latest period, 4.1% of listings saw price increases, down from 9.9% a year earlier.

Source: CBRE Research/ REIDIN

Source: CBRE Research/ REIDIN

Demand within the rental market increased further despite a slowdown in the total number of new registrations

According to data from the Dubai Land Department, the number of rental registrations in the year to date to May 2024 reached a total of 255,178, marking an increase of 5.9% compared to the year prior. This increase has been driven by a 12.2% growth in renewed rental registrations, whereas new contracts registered declined by 3.7%, where we are seeing tenants choosing to renew in situ, as the rate of rental growth in certain typologies and neighbourhoods has significantly weighed on affordability. Source: CBRE Research/ REIDIN

Source: CBRE Research/ REIDIN

Rents will continue to increase in 2024, but not as quickly

The robust levels of demand continue to drive performance in the rental market, where in the year to May 2024, average residential rents in Dubai increased by 21.1%, up from the 20.8% growth registered a month earlier. This increase has been underpinned by a 22.2% rise in average apartment rents and a 13.1% increase in average villa rents. As at May 2024, the average apartment and villa rent stood at AED 126,598 and AED 352,572 per annum, respectively. The highest annual apartment and villa rents were found respectively in Palm Jumeirah, where asking rents reached an average of AED 272,867, and in Al Barari, where rents reached an average of AED 1,391,242. Higher rents within Dubai’s core and prime residential areas have led to a spillover into secondary communities, which are now recording considerable increases in rents on an annual basis. Looking ahead, we expect that rental rates will continue to increase; however, not at the same pace, where already we have been seeing several key and prime residential neighbourhoods heading towards single-digit growth. Affordability constraints are beginning to catch up.

Source: CBRE Research/ REIDIN

Source: CBRE Research/ REIDINFor more market insights, visit our Insights & Research platform.

Briefing Notes

For access to the comprehensive insights discussed in the article, click here to download the briefing notes document.

Connect with an Expert

Share a few details about your request to get started with our team.